Site sections

Editor's Choice:

- The procedure for undergoing medical examinations for employees of children's and educational organizations Law on passing a medical examination for teachers in

- Temple architecture of the ancient Mesopotamia presentation

- Who first invented scuba diving Scuba origin

- Essay on the topic “My future profession

- “Corn, comrades, is a tank in the hands of soldiers!

- Adjustment invoice: registration rules

- Responsibilities of a Manufacturing Supply Manager

- Grants are a means of making dreams come true

- How Belarusian artisans solve the problem of marketing their products. What can an artisan do in Belarus?

- Don Tapping - Lean Office: Eliminating Waste of Time and Money Lean Office Implementation

Advertising

| Can marketing costs be irregular? Creating a marketing budget for the year |

|

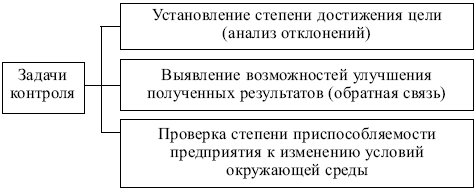

Marketing plan is essential integral part enterprise development plan. This is what the fourth commandment of marketing says: “Well planned is half done.” Marketing Plan– the most important component of the enterprise development plan, a tool for planning and implementing it marketing activities. Strategic Marketing– constant and systematic analysis of market needs, allowing us to determine the most effective products And promising markets with the aim of creating sustainable competitive advantage enterprises. Operational Marketing consists of considering issues of pricing, promotion of goods and organization of their sales. A strategic marketing plan, developed for 3–5 or more years, takes into account marketing opportunities enterprise and contains long-term goals and main marketing strategies, indicating the resources necessary for their implementation. The annual marketing plan includes a description of the current marketing situation, an indication of the goals of marketing activities for the current year and a description marketing strategies necessary to achieve them. A methodological approach to the development of strategic plans was formulated in topic 7. A marketing plan is developed for each strategic business unit and combines plans for individual product lines, individual products, individual markets, individual consumer groups. Strategic and tactical plans for marketing activities have the following sections: Product plan; New product research and development plan; Distribution channel operation plan; Pricing plan; Marketing research plan; Physical distribution system operating plan; Marketing organization plan; Marketing budget is a plan that reflects the projected amounts of income, costs and profits. Along with marketing plans, special programs are being developed aimed at solving individual complex problems: organizing the release of a new product, developing a new market, etc. Such programs can be short-term or long-term and are compiled by working groups specially created for this purpose. Marketing program– a set of interrelated tasks and targeted measures of a social, economic, scientific and technical, production, organizational nature, united by a single goal, indicating the resources used and implementation deadlines. In practice, the following types of marketing activity programs are used: Programs for transferring the enterprise as a whole to work in a marketing environment; Programs for mastering individual elements of marketing activities; Programs for individual directions complex of marketing activities. Of particular interest is market entry program. This program consists of two blocks. Basic block includes: 1) goals and justification for effectiveness: – growth in sales volume; – increase in profit; – acceleration of return on investment; 2) activities in the field of R&D, production, after-sales service, product promotion; 3) resources for individual elements of the marketing mix; 4) plan for implementing activities. IN providing block includes: 1) organizational and economic mechanism for managing the development and implementation of the program - a set of tasks related to: – organizational structure; – personnel; – financing; – remuneration and incentives; 2) information and methodological support: – methods and means of collecting, transmitting, storing and processing information; – methods of program justification; 3) ways to control the implementation of the program. 8.2. Determining Marketing CostsDetermining marketing costs is enough difficult task, because: – marketing costs ensure the process of selling goods; – marketing costs are of an investment nature and can bring income in the near future; – financial planning marketing costs are carried out when developing appropriate budgets (research, communication policy etc.). When determining marketing costs, the following methods are widely used: ? “top-down” - first the total amount of costs is calculated, and then this amount is distributed to individual marketing activities. In this case, the approaches presented in Fig. 1 can be applied. 8.1; ? “bottom-up” - first, the costs of individual marketing activities are calculated, and then these values are summed up using the cost calculation method using the relevant norms and standards (calculations are carried out by the enterprise’s marketing service or by external experts on a contractual basis). Rice. 8.1. Approaches to determining the total amount of marketing costs using the “top-down” method Costs for individual marketing activities are divided into fixed and variable. Fixed marketing costs– costs necessary to continuously maintain operation marketing system at the enterprise. They include costs for: Systematic marketing research; Creation of a bank marketing information for enterprise management; Financing work aimed at improving product range enterprises. Variable marketing costs– costs associated with changes in the market situation and market conditions, the adoption of new strategic and tactical decisions. The marketing service compiles cost estimates in the following areas: Costs of marketing research (topic 3); Costs of developing new products (topic 2); Distribution costs (topic 7); Promotion costs (topic 6). A modern method of planning marketing costs is method of marginal marketing budgets, based on “that the elasticity of consumer response varies with the intensity of marketing efforts.” At the same time, the expenditure of funds on the use of each element of the marketing mix is determined, which leads to the best results (the greatest magnitude of the effect). 8.3. Budget and budgeting in marketingThe marketing budget in quantitative form reflects management's expectations regarding future revenues, financial condition enterprises. The budgeting process requires precision and accuracy, constant clarification. In practice financial management Among the many forms of budgets, the most commonly used are: Flexible budgets – actual and budgeted operations are compared for a given volume of output; Capital budget is a long-term budget intended for the purchase of long-term financial assets; Consolidated budget – consists of production (operating) and financial budgets. The operating budget reflects the planned expenses associated with production activities enterprises. The operating budget includes: –> sales budget - a forecast valuation of expected sales, indicating the expected sales price and sales volume in natural units; –> production budget - the number of units of goods produced, considered as a function of sales and changes in inventory at the end and beginning of the year; –> cost budget for raw materials and supplies – information on the size of purchases of raw materials and supplies for the year; –> factory overhead budget - all types of costs, except for direct labor costs, raw materials and supplies. Consists of variable and fixed overhead costs for the coming year; –> budget for costs of sales and distribution of goods - all sales costs, general and administrative expenses, as well as other necessary operating expenses; –> profit and loss budget. Based on the information contained in all of these budgets, a forward-looking balance is drawn up. 8.4. Control in marketingControl– the final phase of the marketing management cycle, the final link in the process of decision-making and their implementation. At the same time, the control phase is the starting point of a new cycle of marketing management and the implementation of management decisions. The objectives of marketing control are presented in Fig. 8.2.  Rice. 8.2. Objectives of marketing control  Rice. 8.3. Stages of marketing control The following are used forms of control: Strategic control - assessment strategic decisions marketing from the point of view of compliance with the external conditions of the enterprise. Strategic control and audit of marketing is a relatively regular, periodic area of activity of the enterprise’s marketing service; Operational control – assessment of the level of implementation of current (annual) plans. The purpose of such control is to establish compliance of current indicators with planned ones or their discrepancies. Such a comparison is possible provided that the annual plan indicators are distributed by month or quarter. The main means of control: analysis of sales volume, analysis of the company’s market share, analysis of the cost-sales ratio and monitoring of customer reactions; Profitability control and cost analysis - assessment of the profitability of the marketing activities of the enterprise as a whole, in relation to specific products, product groups, target markets and segments, distribution channels, advertising media, commercial personnel, etc. When controlling profitability, the following types of costs are distinguished: –> straight- costs that can be attributed directly to individual elements of marketing: advertising costs, commissions to sales agents, research, wages for marketing employees, etc. They are included in the marketing budget for the relevant areas of activity; –> indirect– costs that accompany marketing activities: payment for rent of premises, transportation costs, etc. These costs are not directly included in the marketing budget, but are taken into account during control. Analysis of the relationship between “marketing costs and sales volume” allows you to avoid significant cost overruns when achieving marketing goals. Objects of marketing control are presented in Fig. 8.4.  Rice. 8.4. Objects of marketing control Identifying marketing costs by element and function is not an easy task. It is usually performed in three stages: 1) study financial statements, comparison of sales receipts and gross profit with current expense items; 2) recalculation of expenses by marketing functions: expenses for marketing research, marketing planning, management and control, advertising, personal selling, storage, transportation, etc. In the calculated table of calculations, the numerator indicates current expense items, and the denominator indicates their breakdown by item of marketing cost. The value of this type of analysis lies in the ability to link current costs to specific types of marketing activities; 3) breakdown marketing expenses by functions in relation to individual products, methods and forms of sales, markets (segments), sales channels, etc. The tabular method of presenting information is usually used: the numerator of the compiled table indicates functional items of expenditure for marketing purposes, and the denominator indicates individual products, markets, specific customer groups, etc. Conducting strategic control and the resulting audit (revision) of marketing strategy unlike the other two forms of marketing control ( operational control and profitability control) is an extraordinary, and often extreme, measure. It is used mainly in cases where: The previously adopted strategy and the tasks it defines are morally outdated and do not correspond to the changed conditions of the external environment; Significantly intensified market positions main competitors of the enterprise, their aggressiveness increased, the efficiency of the forms and methods of their work increased, and this happened in minimum terms; The enterprise suffered a defeat in the market: sales volumes have sharply decreased, some markets have been lost, the assortment contains ineffective goods of low demand, many traditional buyers are increasingly refusing to purchase the enterprise's goods. If managers encounter these difficulties, then a general audit of the entire activity of the enterprise is required, a revision of its marketing policy and practices, perestroika organizational structure, an urgent solution to a number of other serious problems. Audits are necessarily preceded by: A comprehensive analysis of the situation and identification of specific reasons for the unsuccessful operation of the enterprise in the market; Analysis of the capabilities of the technical, production, and sales potential of the enterprise; Determining the prospects for the formation of new competitive advantages. The completed procedures require a revision of the enterprise's strategy, reform of its organizational and management structures, and the formation of new, more difficult tasks and goals that reflect the identified potential opportunities. The types of analysis used in marketing audit are presented in table. 8.1. When auditing the marketing of an enterprise, the following are used: Internal audit – carried out by the enterprise itself; External audit – performed by external experts and audit firms. Table 8.1  Situations to analyze1. Determine what threats and opportunities fast food companies (for example, McDonald's) face in the Russian market. 2. The Tula enterprise “Troika” sets the task: to attract the attention of the population to the products it sells household appliances and by 2004 to ensure a share of the Tula market equal to 50%. Develop a marketing plan. 3. The Tula enterprise "Wallpaper" is widely known in the regional market. However, competition is high. Using the methods of situational analysis and SWOT analysis, identify the company’s opportunities to strengthen its competitive advantages. 4. OJSC Avtoshina, well-known in the motor oil market, decides to conduct an external audit. Are the costs of an audit justified for a thriving company? 5. The owner of the Orange restaurant believes that his activities are not sufficiently profitable. How can marketing control help him run his business more successfully? 6. Does senior management need educational institution conducting periodic marketing audits? If yes, then create a plan to audit your marketing activities. 7. Based on the following data, draw up a production budget at the end of the year: – product sales volumes – 10,000 units; – sales unit price – 22 rubles; – the desired amount of inventory at the end of the year is 1150 units; – enterprise inventories at the beginning of the period – 1000 units. Based on the data provided, create a sales budget. Marketing costs should initially be divided:

IN general view The structure of marketing costs is shown in Fig. 1.5. At the same time, the costs associated with marketing activities are also heterogeneous, for example, the costs of advertising in print media mass media(media) consist of different types costs: content development, original layout creation, placement. And while not every cost group can be managed, each needs to be tracked. Rice. 1.5. Profit can be planned, and the actual profit received can be calculated. This is already the function of an accountant. Not all expenses can be taken into account in the income tax base. Therefore, there are costs that reduce the tax base only partially, within the limits of the norms. And therefore marketers need to remember that expenses, from this (accounting) point of view, can be standardized (limited in size) and non-standardized (unlimited and fully taken into account in the cost price). Accounting for such expenses has its own peculiarities. Marketing and advertising expenses, as well as expenses for management activities, reduce taxable income. However, these costs are difficult to control, so controllers have a lot of complaints about marketing costs. And marketers should know this when creating a marketing budget. The main reasons for refusals by tax authorities to recognize such expenses is the lack of economic effect in confirming expenses 1 . For example, if marketing research ordered externally does not produce results, then it will be difficult for the organization to defend its case.

Example 1.5. The company's revenue for a certain period amounted to 1000 thousand rubles. During this period, the company spent 200 thousand rubles on marketing. At the same time, 100 thousand rubles. classified as non-standardized. Answer: 100 + 1000 -0.01 = 110 thousand rubles. In other words, 90 thousand rubles. the company will pay from profits, so it must carefully analyze advertising expenses and try include them in non-standardized ones. The feasibility of many costs for marketing activities raises many questions. Most Western methods and techniques for promoting sales in Russian conditions They simply don’t work or give a negative result. Many experts often ask the question: at what stage of business development are the costs of analytical marketing economically justified? The answer, in their opinion, depends on the size of the company’s product line, the degree of its diversification, financial opportunities and perhaps ambition. At the same time, company managers also face other acute problems related to marketing costs, such as the optimality of the advertising budget, the costs of sales activities, and the place of these costs, mostly as part of indirect costs. The inclusion of these costs in indirect (fixed costs) is not entirely correct, but this greatly simplifies the calculation (Fig. 1.6).  Rice. 1.6. Example 1.6. Let's look at the data in Example 1.5. Variable costs - 1000 rub. Fixed costs - 20,000,000 rubles. Additional marketing expenses - RUB 3,000,000. Investments - 100,000,000 rubles. The expected return on investment is 10%. The planned sale price is 2500 rubles. How many products do you need to sell to get the required amount of profit, pay employees wages, pay bills and offset marketing expenses? From here N-22 000 products. Therefore, to compensate for the additional marketing costs, an additional 2,000 products must be manufactured and sold. Marketers need to remember this. Any marketing expenses should be offset by an increase in projected sales. Let's consider the costs associated with the organization and maintenance of the marketing service (department) (see Fig. 1.5). These costs include:

The budgeting process requires precision and accuracy, constant clarification. In the practice of financial management, among the numerous forms of budgets, the most commonly used are:

The operating budget reflects the planned expenses associated with the production activities of the enterprise. The operating budget includes:

Based on the information contained in all of these budgets, a forward-looking balance is drawn up. Control in marketingControl is the final phase of the marketing management cycle, the final link in the process of decision-making and their implementation. At the same time, the control phase is the starting point of a new cycle of marketing management and the implementation of management decisions. The objectives of marketing control are presented in Fig. 8.2.

The following forms of control are used:

When controlling profitability, the following types of costs are distinguished:

Analysis of the relationship between “marketing costs and sales volume” allows you to avoid significant cost overruns when achieving marketing goals. Objects of marketing control are presented in Fig. 8.4.

Identifying marketing costs by element and function is not an easy task. It is usually performed in three stages:

the numerator of the compiled table indicates functional items of expenditure for marketing purposes, and the denominator indicates individual products, markets, specific customer groups, etc. Conducting strategic control and the resulting audit (revision) of the marketing strategy, in contrast to the two other forms of marketing control (operational control and profitability control), is an extraordinary and often extraordinary measure. It is used mainly in cases where:

If managers are faced with these difficulties, then a general audit of the entire activity of the enterprise is required, a revision of its marketing policies and practices, restructuring of the organizational structure, and an urgent solution to a number of other serious problems. Audits are necessarily preceded by:

The completed procedures require a revision of the enterprise's strategy, reform of its organizational and management structures, and the formation of new, more difficult tasks and goals that reflect the identified potential opportunities. The types of analysis used in marketing audit are presented in table. 8.1. When auditing the marketing of an enterprise, the following are used:

Table 8.1

Managers must understand which marketing costs will always remain the same and which will change as sales volumes change. The classification of distribution costs will depend on the organizational structure and on specific management decisions. However, a number of items typically fall into one category or another. Marketers often don't consider their budgets in terms of fixed and variable costs, but by doing so they could gain at least two benefits. Marketing expenses are often the largest portion of a company's discretionary expenses. Essentially they are important factors short-term profit. Of course, marketing and sales budgets can also be viewed as investments in attracting and retaining client base. However, in either approach, it is useful to distinguish fixed marketing costs from variable marketing costs. In other words, managers need to understand which marketing costs will always remain the same and which ones will change as sales volumes change. This classification would require an itemized review of the entire marketing budget. Usually gross variable costs are considered as expenses that change with changes in the volume of unit sales. Regarding distribution costs a slightly different concept will be needed. Instead of varying with changes in unit sales, total variable distribution costs are likely to change directly with the value of units sold, that is, with changes in income. Thus, most likely, variable distribution costs will be expressed as percentage of income, and not as a certain part of the monetary value of a unit of goods. The classification of distribution costs (fixed and variable) will depend on organizational structure and from specific management decisions. However, a number of items usually fall into one category or another - provided that their status as constants or variables may vary over time. Ultimately, all costs become variable. During quarterly or annual planning period fixed costs Variable expenses marketing may include: Marketers often don't consider their budgets in terms of fixed and variable costs, but by doing so they could gain at least two benefits.

Total distribution costs (marketing costs) ($) = Total fixed distribution costs ($) + Total variable distribution costs ($) Total variable distribution costs ($) = Income ($) * Variable distribution costs (%) Trading commission costs. Sales commissions are one example of distribution costs that vary with income. Therefore, any sales commissions should be included in variable selling costs.

There are many types of variable distribution costs. For example, distribution costs may be calculated using complex formulas specified in companies' contracts with brokers and dealers. Selling costs may include incentives to local dealers based on meeting sales targets. They may also include promises to reimburse retailers for joint advertising costs. What to pay attention to Fixed costs are often easier to measure than variable costs. Typically, fixed expenses can be compiled from payroll records, lease documents, or financial statements. To determine variable costs it is necessary measure the rate of their increase. Although variable distribution costs are often a predetermined percentage of revenue, they can alternatively vary with changes in the number of units sold (as is the case with a packaging discount). A further complication arises if some variable distribution costs relate to only a portion of total sales. This can happen, for example, when some dealers receive cash discounts or preferential rates for a certain shipment of goods, while others do not have such privileges. Things get more complicated when some costs may appear to be fixed when in fact they are incremental. That is, they are constant up to a certain point, and then they trigger additional costs. For example, a company may enter into a contract with advertising agency for three advertising campaigns per year. If she decides to pay for more than three campaigns, this will incur incremental costs. Typically, incremental costs can be treated as fixed costs, provided the boundaries of the analysis are well understood. Staged payments are sometimes difficult to model. Discounts for customers whose purchases exceed a certain level, or bonuses for sales staff who exceed sales quotas, can be difficult to describe features. Creativity is important when planning marketing discounts, but such creativity can sometimes be difficult to capture within fixed and variable costs. When developing its marketing budget, a company must decide how much of its expenses should be allocated to the current period and how much to amortize over several periods. This rate is suitable for costs that are considered as capital investments. An example of such an investment would be a discount on the financial debt of new distributors. Rather than adding such a discount to the current period budget, it would be better to view it as a marketing item that increases the company's investment in working capital. Conversely, advertising costs intended to generate long term impact, can hardly be called an investment; It makes more sense to consider them marketing expenses. Important indicators and concepts Marketing spend levels are often used to compare companies and to demonstrate how much they are investing in a given area. Therefore, marketing expenses are usually viewed as a percentage of sales. Marketing costs as a share of sales. The level of marketing expenditure expressed as a share of sales. This figure shows how actively the company is engaged in marketing. The appropriate level of this indicator varies depending on the type of product, strategies and markets. Marketing costs as a share of sales (%) = Marketing costs ($) / Revenue ($) Variations of this metric are used to test marketing elements against sales volume. Examples include incentives targeting the sales area, measured as a percentage of sales, or incentivizing in-house sales personnel as a percentage of total sales. Advertising costs as a percentage of sales. Advertising expenses as a share of sales. It is typically a subset of marketing expenses expressed as a percentage of sales. Before using such metrics, marketers are advised to determine whether certain marketing expenses have been deducted when calculating sales revenue. Retail discounts, for example, are often subtracted from gross sales to calculate net sales. Deductions per place. This is a special form of distribution cost that is encountered when new quantities of goods are brought in to retailers or distributors. They are essentially fees that retailers pay for providing space for new products in their stores and warehouses. These deductions can take the form of one-time cash payments, free merchandise, or special discounts. The exact terms of the space fee will determine whether it constitutes a fixed cost, a variable cost, or a combination of both. Understanding the difference between fixed and variable distribution costs can help companies consider the relative risks associated with alternative distribution strategies. In general, strategies that incur variable distribution costs are less risky because variable distribution costs will remain lower if sales do not meet expectations. In previous articles in our magazine devoted to the marketing function, we touched on a number of organizational issues: the structure of the marketing service, job descriptions of employees of marketing departments, etc. The next topic is the determination of marketing costs. We included this topic in this issue based on the following arguments. Most firms are now experiencing resource constraints. There may, of course, be exceptions, but austerity is dominant financial resources exists. In this situation, it becomes quite possible to shift marketing costs to “later”, partly due to a lack of understanding of the importance of this management function, partly due to a lack of knowledge in the field of maneuvering resources within the marketing function. In this regard, when preparing an article for this issue, we asked our clients to send us their marketing budgets broken down by item. The results of the generalizations we have made, as well as additions from statistics from the American Bank Marketing Association, the American Apparel Manufacturers Association, and the American Retail Merchants Association, are before you. Perhaps some cost items may seem irrelevant to you in your circumstances. It's OK. Just put "0" against these lines for now, but rest assured that sooner or later they will be useful to you. So, marketing is aimed at creating and maintaining a positive image of the organization, maximizing the use of its resources to identify, promote and satisfy market needs for products and services on a profitable basis. In this context, from the standpoint of determining cost items, 4 blocks can be distinguished within the marketing function:

a) motivating the customer to purchase or use a product-service that provides benefits, guarantees or satisfaction to the user, b) transfer of information aimed at strengthening the reputation or position of the advertiser. B. Marketing Research. The use of various methods and means on a permanent and systematically to analyze information related to: Who are existing and potential clients? Geography of client placement. What products and/or services does the client want and which ones does he really need? Where the client prefers to receive services or how and when they should be provided. What are the conditions of competition? B. Public Relations. A permanent and ongoing program of activities designed to involve a firm in the social, cultural, educational, environmental and economic life of a region or larger administrative entity (for example, a country). D. sales promotion. A set of actions to enhance the effectiveness of advertising and customer contact programs by increasing awareness and knowledge of products or services at the point of sale. We present these well-known truths with one single purpose - to connect the upcoming lists of costs with the above marketing blocks. Now let's move on to cost items. 7. Acquiring space at trade shows, fairs, etc. 15. Costs for photographs and payment for models participating in advertising. 17. Posters, displays, etc., placed within the company for advertising purposes. MARKETING RESEARCH COSTS 1. Research on advertising pre-testing and advertising effectiveness. 2. Payment for marketing research consultants. 3. Research related to the introduction of new products and services. 4. Research related to the company's image; public opinion research. 5. Quarterly, semi-annual and annual sample market research for penetration and perception. 6. Testing and evaluation of sales promotion activities. Ultimately, all costs are aimed at conducting research on the potential of new products and services, market share, the selection of branches and affiliates, the image of the company, the effectiveness of advertising and preliminary testing of proposed public relations projects. PUBLIC RELATIONS COSTS 2. Celebrating anniversaries and significant dates. 4. Awards given in charitable events. 5. Calendars. 6. Greeting cards. 7. Financing of events carried out by municipal authorities. 8. Donations and subsidies. 9. Production of displays for the needs of municipal authorities. 10. Payment of public relations consultants. 11. Payment for special events offered to the public. 12. Gifts and souvenirs with the organization’s logo. 14. Letters of gratitude clients for agreeing to do business with the company, various types of congratulations and their mailing. 15. Production of geographical maps with the company logo and its location. 16. Costs of holding an open house day for the company. 17. Sponsoring of creative and sports groups and cultural/sports events. 18. Press conferences. 19. Costs of scholarships. 20. Costs of weather and time systems for installation in public places without a company logo. 21. Costs of external speech writers. 23. Development trademark or company logo. COSTS FOR SALES PROMOTION (a separate group of costs aimed at expanding knowledge about the company’s products and services both externally and internally). 1. Audiovisual materials, including slides, audio and video cassettes for demonstration during speeches related to the sale of products and services. 2. Production of items (banners, boxes, etc.) for use at points of sale of products and services. 3. Souvenirs for clients starting business with the company. 4. Prizes or bonuses for employees who attract new clients. 5. Letters related to increasing sales volumes and their mailing. 6. Training of personnel related to the sale of products and services. 7. Organizing meetings with new clients |

Popular:

New

- Temple architecture of the ancient Mesopotamia presentation

- Who first invented scuba diving Scuba origin

- Essay on the topic “My future profession

- “Corn, comrades, is a tank in the hands of soldiers!

- Adjustment invoice: registration rules

- Responsibilities of a Manufacturing Supply Manager

- Grants are a means of making dreams come true

- How Belarusian artisans solve the problem of marketing their products. What can an artisan do in Belarus?

- Don Tapping - Lean Office: Eliminating Waste of Time and Money Lean Office Implementation

- How to correctly find out about the results of an interview: expert advice How to ask an employer about a decision